Adjusting for inflation - College

Adjusting for inflation

Inflation adjustments added to your pension can help preserve your buying power throughout your retirement.

Your future pension payments may increase from time to time thanks to cost-of-living adjustments (COLAs). A COLA is a small annual increase added to retired members’ pensions to help keep pace with increases in the cost of living.

COLAs are not a guaranteed benefit, so you may not receive a COLA each year, and the amount may change from year to year. However, once you receive a COLA, it becomes part of your basic lifetime monthly pension. When approved, COLAs are also applied to the bridge benefit and temporary annuity portion of your pension, if applicable.

Each year, the College Pension Board of Trustees carefully considers various factors to decide whether to approve a COLA and, if so, its value.

To understand how this works, it helps to know that your pension is funded through two accounts: the basic account and the inflation adjustment account.

Member and employer contributions and investment returns fund the basic account. Your basic pension is paid each month from funds in the basic account.

Source: BCPC Finance 2020

Inflation adjustment account = funding for COLAs

The inflation adjustment account is separate from the basic account. Member and employer contributions and investment returns also fund this account. COLAs are not guaranteed; the board decides whether to approve a COLA based on the funds available in the inflation adjustment account.

After a COLA is approved, funds from the inflation adjustment account are transferred to the basic account so they can be applied to your basic pension, bridge benefit and temporary annuity, if applicable.

Calculating COLAs

The board is dedicated to ensuring COLAs are sustainable over the long term. Each year, the board examines several factors to decide whether to grant a COLA. If the board grants a COLA, it takes effect the following January.

The board makes its decision based on:

- The annual change in the 12-month average Canadian consumer price index

- The COLA cap

- The funds available in the plan's inflation adjustment account

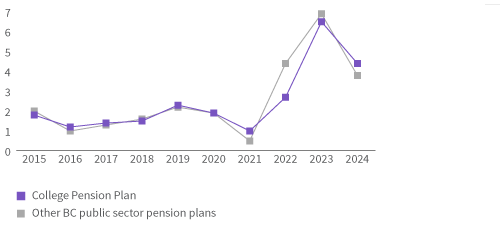

You may have noticed some pension plans have COLA amounts that are different from yours. That’s because BC public sector pension plans have different ways of calculating the COLA. In general, different calculation methods generate different annual COLA amounts. The good news is that no method produces results that are consistently higher or lower than the others over multiple years.

Calculation methods

The COLA is calculated using monthly rates from the Canadian consumer price index (CPI).

Your plan uses the annual percentage change in the average CPI. With this method, the COLA is based on the annual percentage change in the 12-month average CPI from one year to the next. Each year, that average, from November to October, is compared to the average for the 12-month period that came before it. The difference between the two 12-month periods becomes the COLA.

Other BC public sector pension plans may use the percentage change between September CPIs. In this method, the COLA is based on the percentage change between the current year’s September CPI and the previous September’s CPI.

Example

In some years, one method generates a higher COLA/inflation adjustment; in some years the other method generates a higher amount.

COLA methodologies comparison (%)

Because of COLA/inflation adjustment caps, some plans did not grant the full COLA/inflation adjustment amounts determined by their plan's methodology in certain years.

COLA caps

The COLA cap is the maximum amount of COLA that can be granted each year, expressed as a percentage. Capping the annual COLA amount helps maintain the long-term sustainability of funds in the inflation adjustment account by making sure they are not used up faster than they can be replaced. That’s why the plan rules and funding policy specify:

- The cost of providing COLA cannot exceed the funds in the inflation adjustment account

- The amount of COLA cannot exceed the lesser of:

- the increase in CPI

- the COLA cap

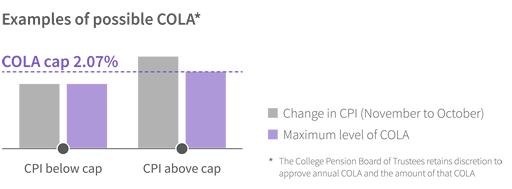

The example below shows how a COLA cap of 2.07 per cent would affect your pension. If the increase in the CPI was less than 2.07 per cent, you would receive a COLA equal to the CPI. If the increase in the CPI was more than 2.07 per cent, you would receive a COLA of 2.07 per cent.

For 2021 and 2022, the COLA cap has been suspended. That means if a COLA is granted, the amount may be equal to the average increase in the CPI. However, the board must still consider the funds available in the inflation adjustment account when setting the COLA amount.

At any time, the board may choose to reintroduce the cap on the maximum COLA to protect its sustainability.

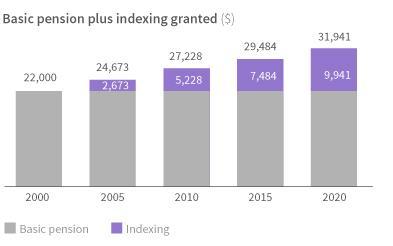

COLAs add up over time. For example, if you started receiving an annual pension of $22,000 in 2000, your annual pension in 2020 would be $31,941 as a result of COLAs approved by the board.